SBA Opens a Narrow Waiver Path for Minority Investors With Prior SBA Loss Issues

Eric Pacifici

May 29, 2026

Passive minority investors with prior SBA-loss history may now have a path forward in certain SBA-financed acquisitions. The catch is that the new guidance is narrower than it sounds.

If you raise minority capital for SBA-financed acquisitions, or you write small checks into other people’s SBA deals, this one is worth two minutes. SBA has created a potential discretionary waiver for certain non-controlling minority equity investors who got connected to a prior SBA loss. It is good news. It is not a blanket fix, and it is not automatic approval.

Here is the practical version.

What Changed

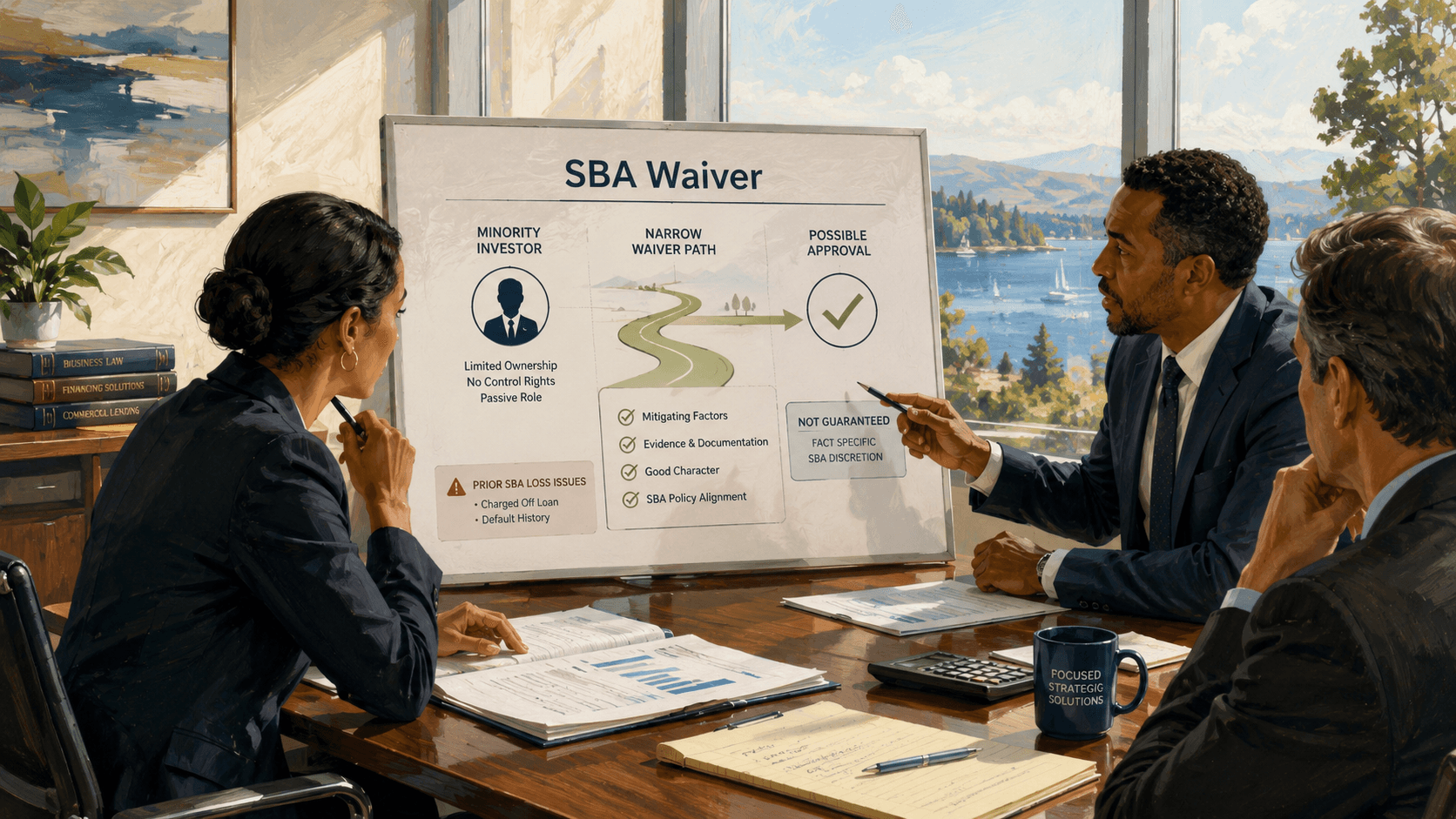

SBA has opened a discretionary waiver path for certain passive, non-controlling minority equity investors who are tied to a prior SBA loss.

The change comes through SBA Policy Notice 5000-879464, effective June 1, 2026, covering both 7(a) and 504 loans. In plain terms: SBA may now, on a case-by-case basis, let an otherwise eligible applicant get an SBA loan even when one of its owners was associated with a business that caused a prior SBA loss, as long as that owner’s role was genuinely passive and their stake is small.

That is the whole shift. SBA did not eliminate the prior loss rule. It created a narrow lane to ask for relief from it.

Why Minority Investors Were Worried

The prior loss rule has a long reach. If an applicant, or any of its owners, previously owned or controlled a business that defaulted on a federal loan and cost the government money, that history could sink eligibility for the next deal. A compromise agreement counts as a loss too.

Read literally, that swept in passive investors. Hold a small, hands-off stake in a company that later went bad, and that loss could follow you into your own acquisition years later. You did not run the company. You did not sign the note. You still got caught in the net.

That risk made experienced searchers, HoldCo operators, and investors nervous about taking or accepting minority positions. Nobody wants one bad outcome in a small, passive position to quietly poison their SBA eligibility down the road. This update appears to recognize that a passive minority investor should not be treated the same as an owner-operator who actually controlled the company and the loan.

Who May Qualify

This is built for a narrow fact pattern. The investor generally needs to clear all of the following.

In the business that caused the prior loss:

· Owned less than 20% of that business.

· Was not a guarantor or co-borrower on the defaulted SBA loan.

· Had no control over that business.

In the current deal:

· Holds a non-controlling ownership interest of less than 20% in the new applicant.

Miss one of these, and you may be outside the waiver lane. This is for genuinely passive minority positions, not for operators trying to relabel a deal they ran.

Even when all of that is met, SBA still looks at the full picture. That includes the investor’s involvement with prior SBA loan defaults, the timing of the default, how many prior losses exist, and the size of the investment relative to the SBA loan amount. Clearing the criteria gets you considered. It does not get you approved.

One mechanics note worth knowing: this is not a separate standalone waiver application that automatically fixes the issue. The issue still needs to be raised with the lender, submitted through the lender’s process, and reviewed by SBA. That is why buyers should flag the issue early, before the loan package is deep into underwriting.

What Has Not Changed

Read this part carefully, because the headline is more generous than the rule.

· Prior SBA losses still matter.

· The waiver is discretionary. SBA may consider it. SBA is not required to grant it.

· SBA reviews the facts case-by-case, every time.

· Control, guarantor status, co-borrower status, and ownership percentage all still matter.

· This does not appear to apply to PPP loans, COVID EIDL loans, or defaults on other federal or non-SBA debt.

As prominent SBA lender-side attorney Scott Oliver of Lewis & Kappes, P.C. put it, the update reflects “the SBA continuing to tighten certain credit and eligibility standards while also recognizing that modern capital structures and investment arrangements do not always fit neatly into older eligibility frameworks.” Oliver summarized the practical impact this way: “The SBA appears to be recognizing that a passive minority investor should not automatically be treated the same as an owner/operator who controlled the company and the loan.” But, as Oliver also cautioned, “this is not an automatic approval.”

What Buyers Should Do Now

“This is a helpful clarification for SBA acquisition financing, but buyers should not treat it as an automatic fix,” said Eric Pacifici, Partner at SMB Law Group. “The waiver remains discretionary, and we do not yet know how consistently the SBA will apply it in practice. The right move is to identify these issues early, document the investor’s non-controlling role, and coordinate with the lender before the deal is deep into underwriting.”

If you have an investor in the mix, run this short checklist before you get far into a deal:

· Ask investors early whether they have been connected to any prior SBA loan defaults or losses.

· Confirm whether the investor was a guarantor, co-borrower, operator, manager, control person, or purely passive.

· Confirm the investor’s ownership percentage in both the prior business and the new applicant.

· Discuss the issue with the SBA lender before finalizing the cap table or submitting the loan package.

· Do not assume the waiver will be granted.

· Build time into the deal timeline for lender and SBA review if the issue exists.

Bottom Line

Passive minority investors with prior SBA-loss history may now have a path forward. But only if the facts fit, the issue is raised properly, and SBA exercises its discretion to grant the waiver.

It is a real shift, not a free pass. If you have a deal where an owner has any prior SBA loss in their history, treat it as a structuring conversation to have before you sign, not an afterthought during underwriting.

---

SMB Law Group LLP is a transactional M&A boutique representing ETA buyers, HoldCo operators, independent sponsors, and founders across 12 states. We have closed over 380 deals representing $1.8 billion in transaction value. For questions about how the prior loss waiver affects your structure, reach out to our team.

Disclaimer. This article is for general informational purposes only and does not constitute legal, tax, or financial advice. Reading or sharing it does not create an attorney-client relationship between you and SMB Law Group LLP or any of its attorneys. SBA rules, SOPs, and guidance are subject to change. Any deal structure depends on the specific facts, jurisdiction, and counterparty terms involved. Prior results do not guarantee a similar outcome.

SMB Law Group LLP is a Texas limited liability partnership with its principal office at 270 N Denton Tap Rd, Suite 100, Coppell, TX | smblaw.group. The firm is licensed to practice in CA, CO, FL, GA, IL, MA, MI, MN, NC, NY, OH, TX, and UT. Attorney responsible for this content: Eric Pacifici.

Our Blog

More Recent Posts

Ready to Protect and Grow Your Business?

Get experienced legal guidance tailored to your business needs. Schedule a consultation with our team today.